Your browser is out-of-date!

For a richer surfing experience on our website, please update your browser. Update my browser now!

For a richer surfing experience on our website, please update your browser. Update my browser now!

The portfolio is the assimilation of the semester work under the studio “Strategic Plan for Urban Transport Systems”. Through the case city of Ahmedabad, the process of making the long-term urban transportation plan including its linkage with socio-economic and spatial aspects of the city was understood.

The studio framework consisted of reviewing the existing transportation plan across India and abroad. The objective was to learn different methodologies involved in the existing situation analysis. It also helped in gaining insights into proposal formulation. The second step was to study the data collection of the case city of Ahmedabad. Due to the covid limitations, secondary sources and the HH surveys conducted in 2012 and 2019 were considered. The analysis helped to identify the issues of the transport system. Lastly, different growth concepts were derived which helped in defining the overall strategic plan for 2041.

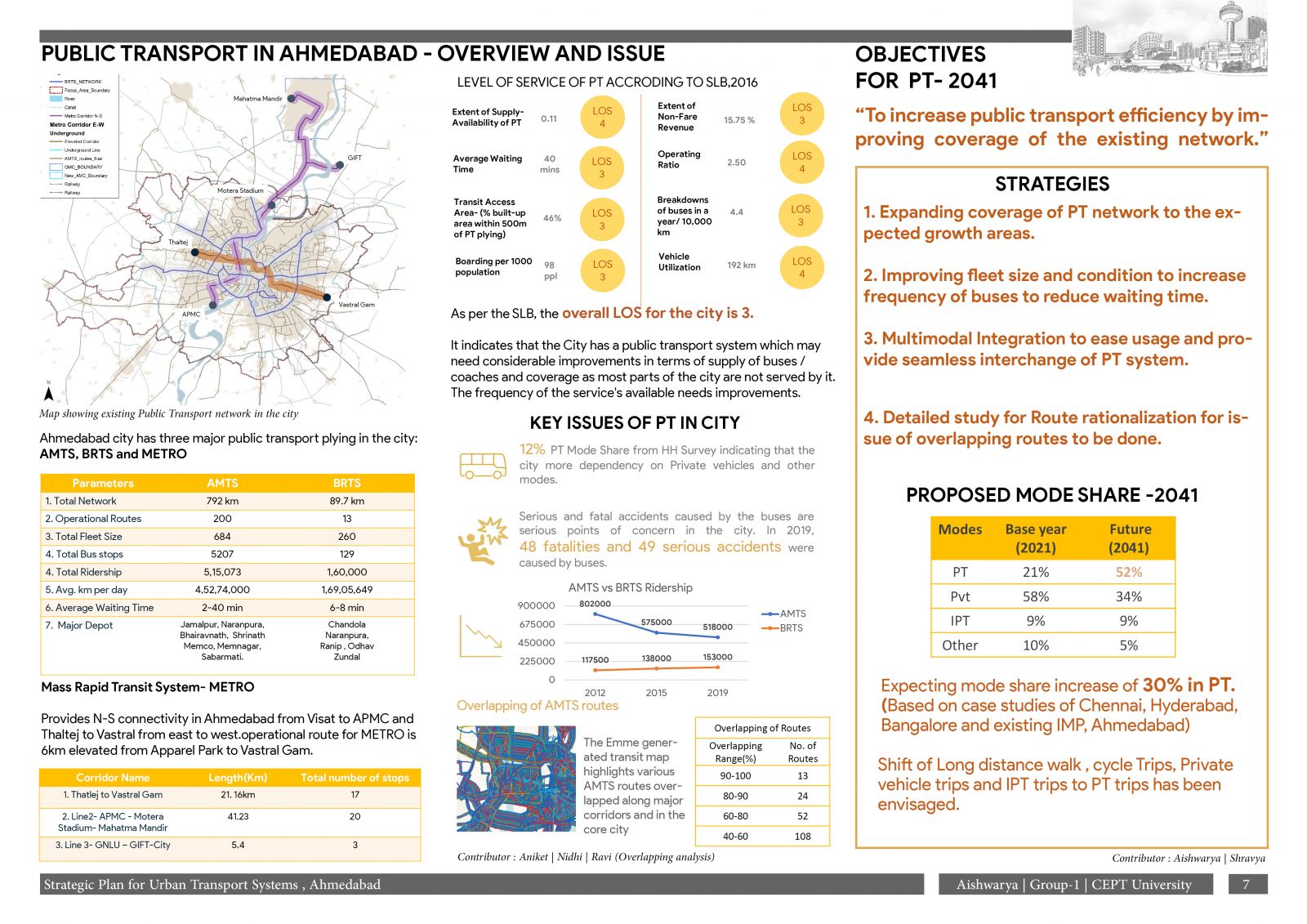

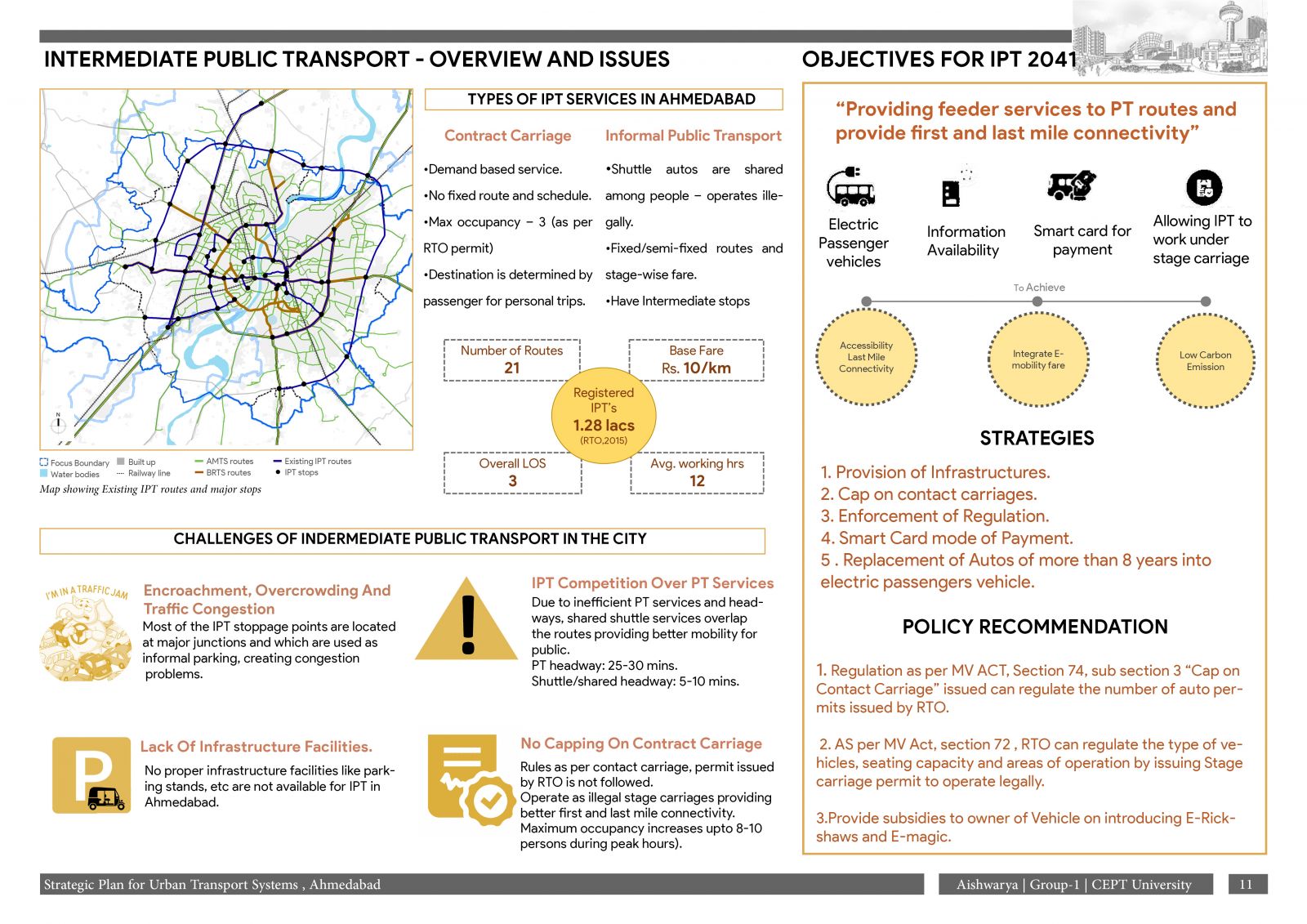

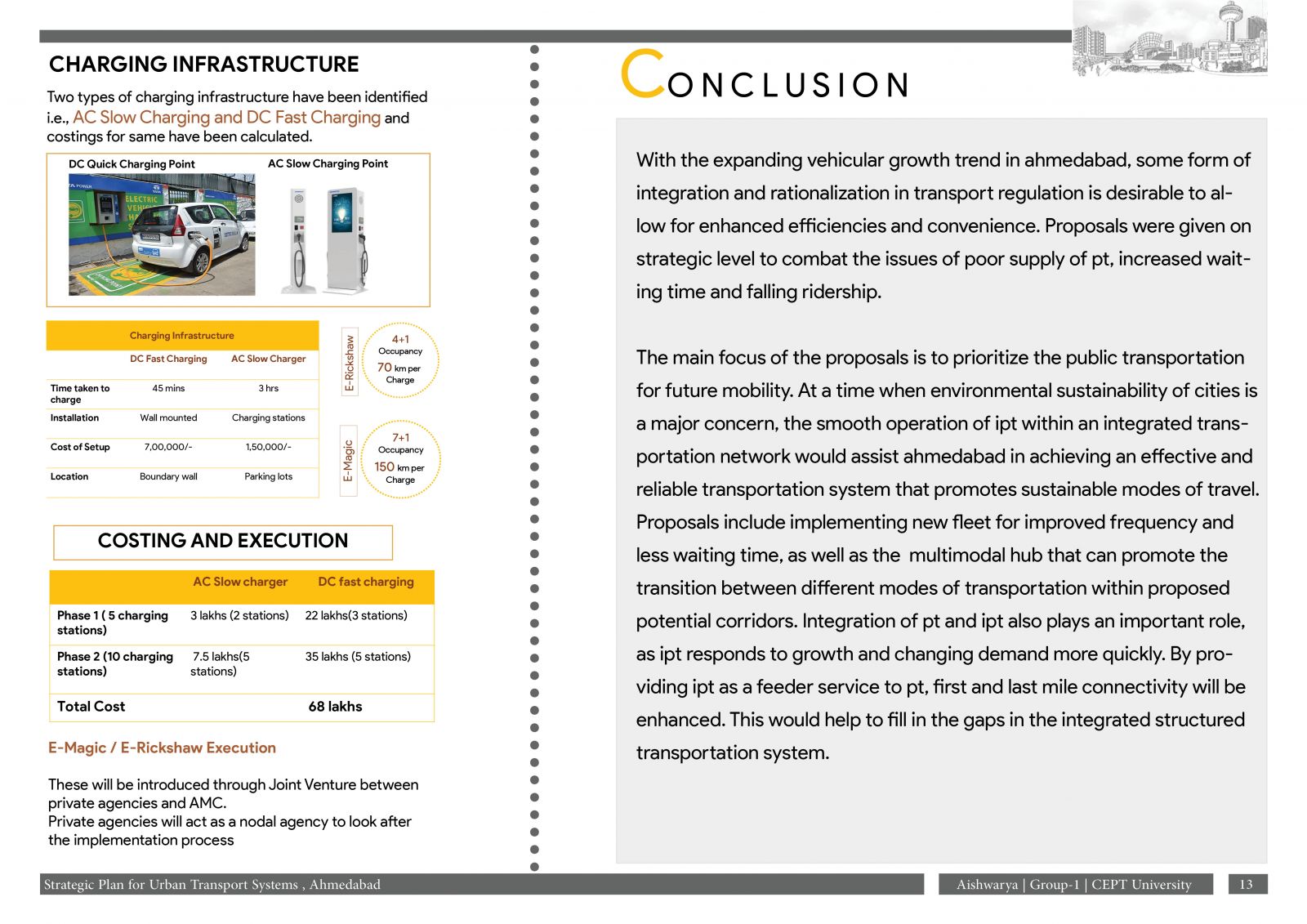

With the expanding vehicular growth trend in Ahmedabad, some form of integration and rationalization in transport regulation is desirable to allow for enhanced efficiencies and convenience. Proposals were given on a strategic level to combat the issues of Poor supply of PT, increased waiting time and falling ridership.

The main focus of the proposals is to prioritize Public transport for future mobility. At a time when the environmental sustainability of cities is a key concern, the smooth functioning of IPT within an integrated transport network will help Ahmedabad to achieve an efficient and reliable transport system that would promote sustainable modes of travel.