Your browser is out-of-date!

For a richer surfing experience on our website, please update your browser. Update my browser now!

For a richer surfing experience on our website, please update your browser. Update my browser now!

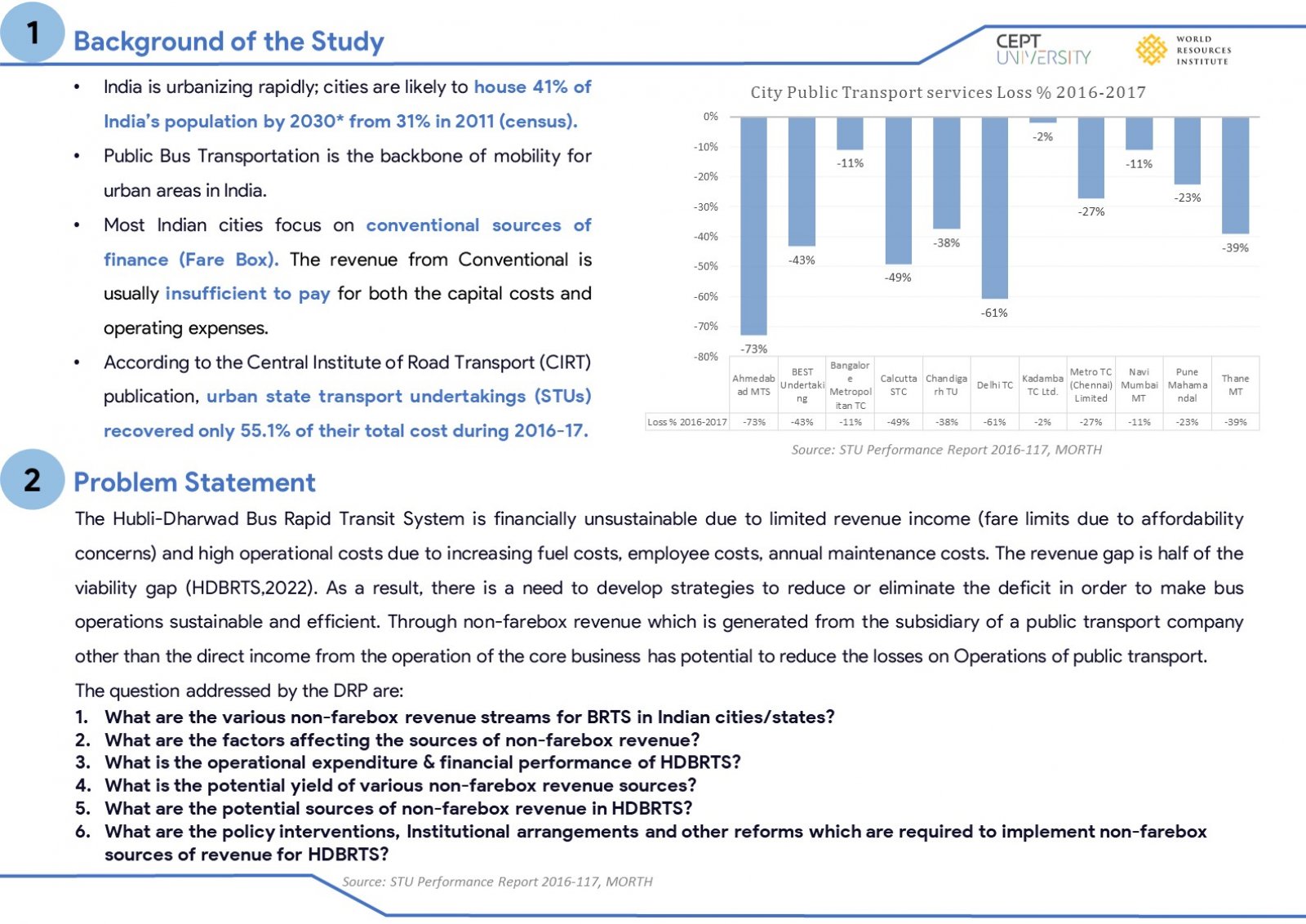

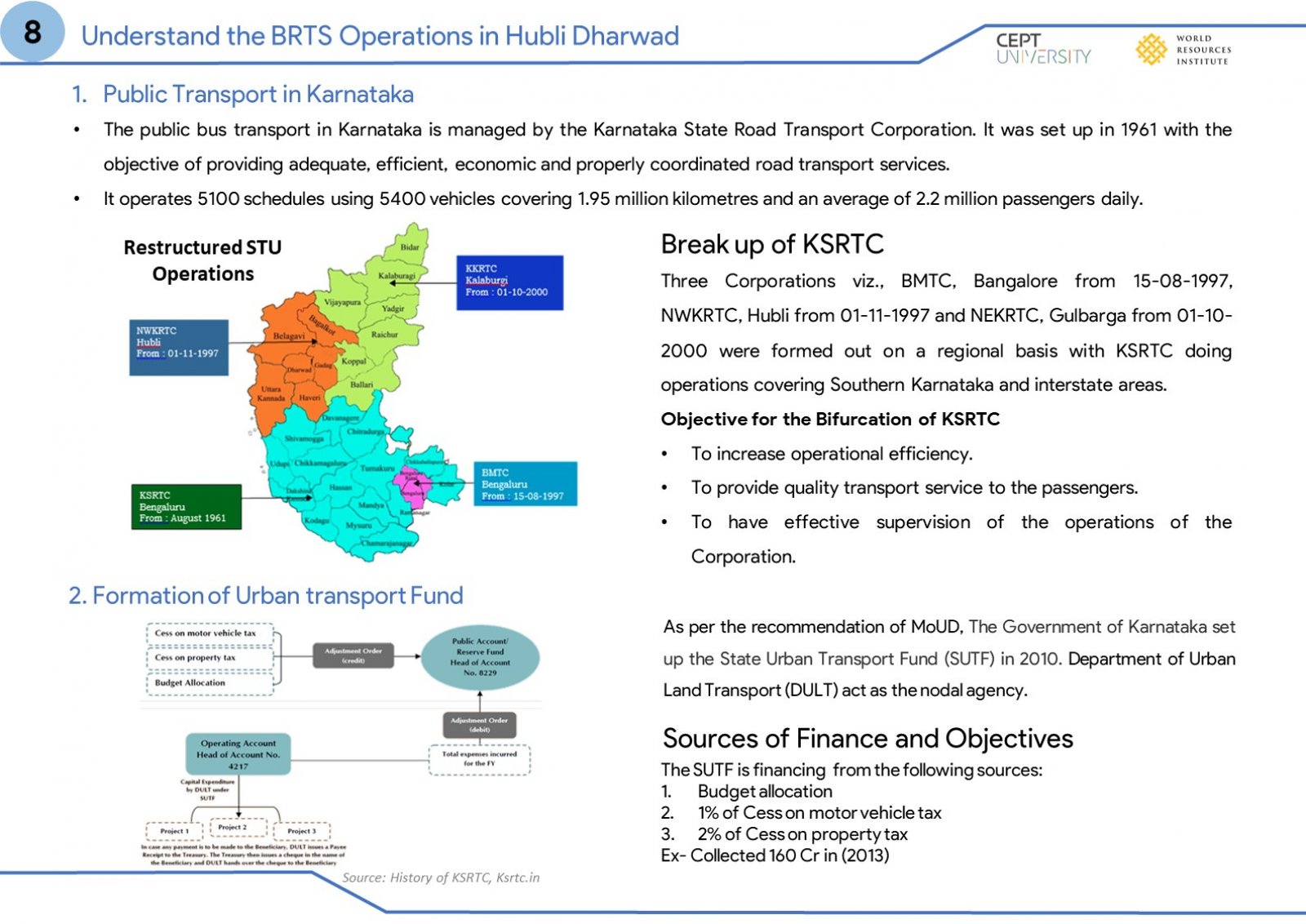

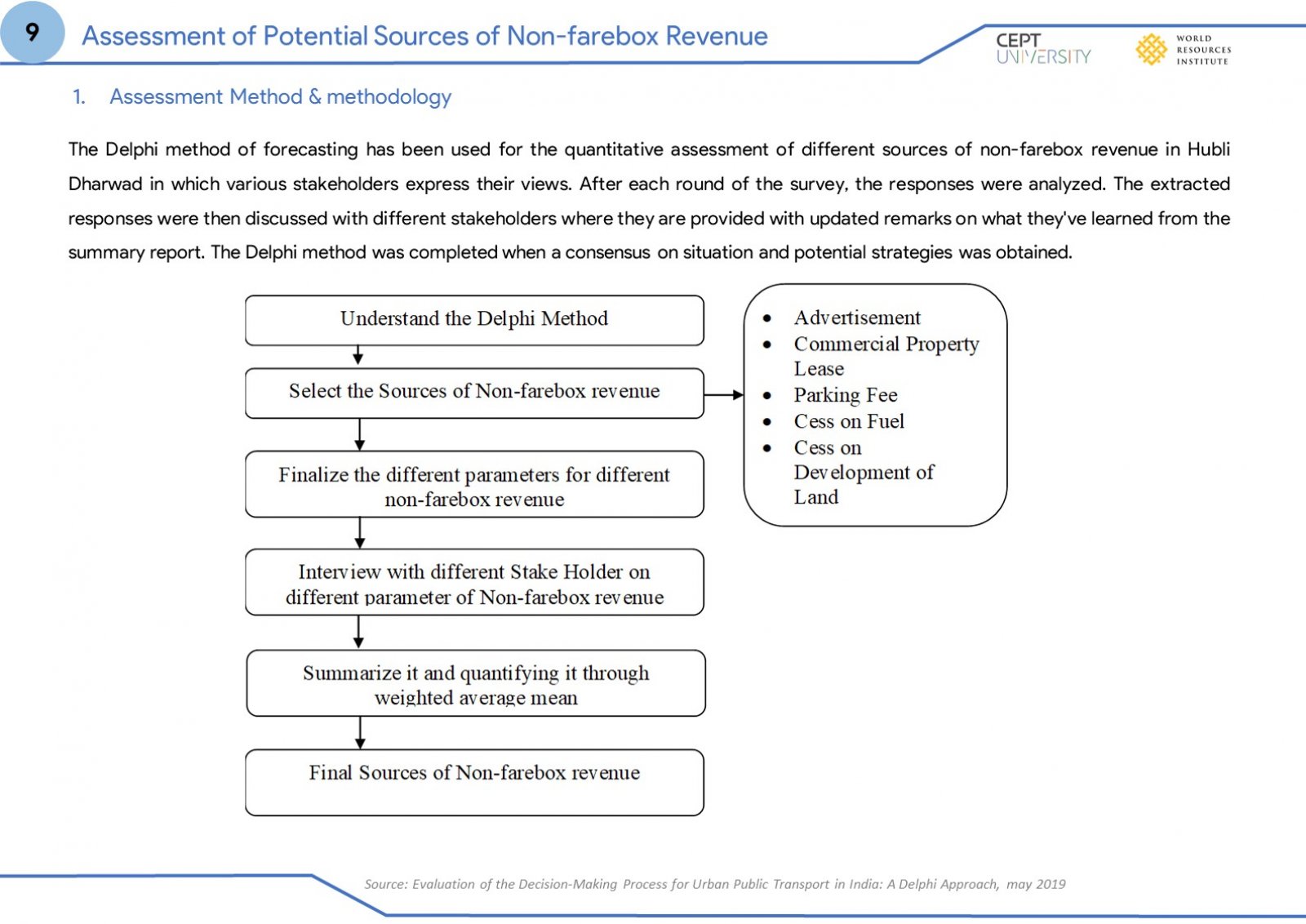

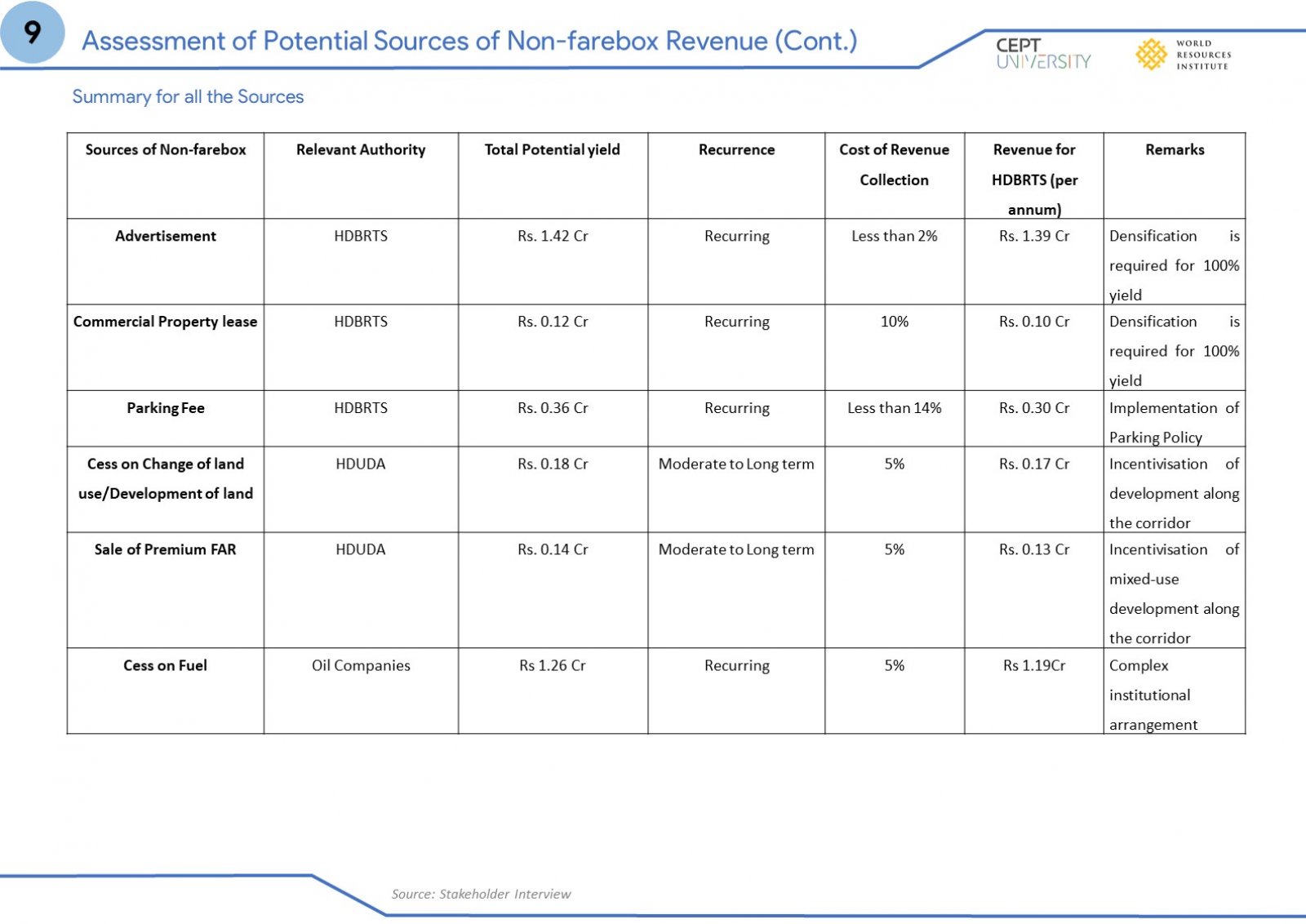

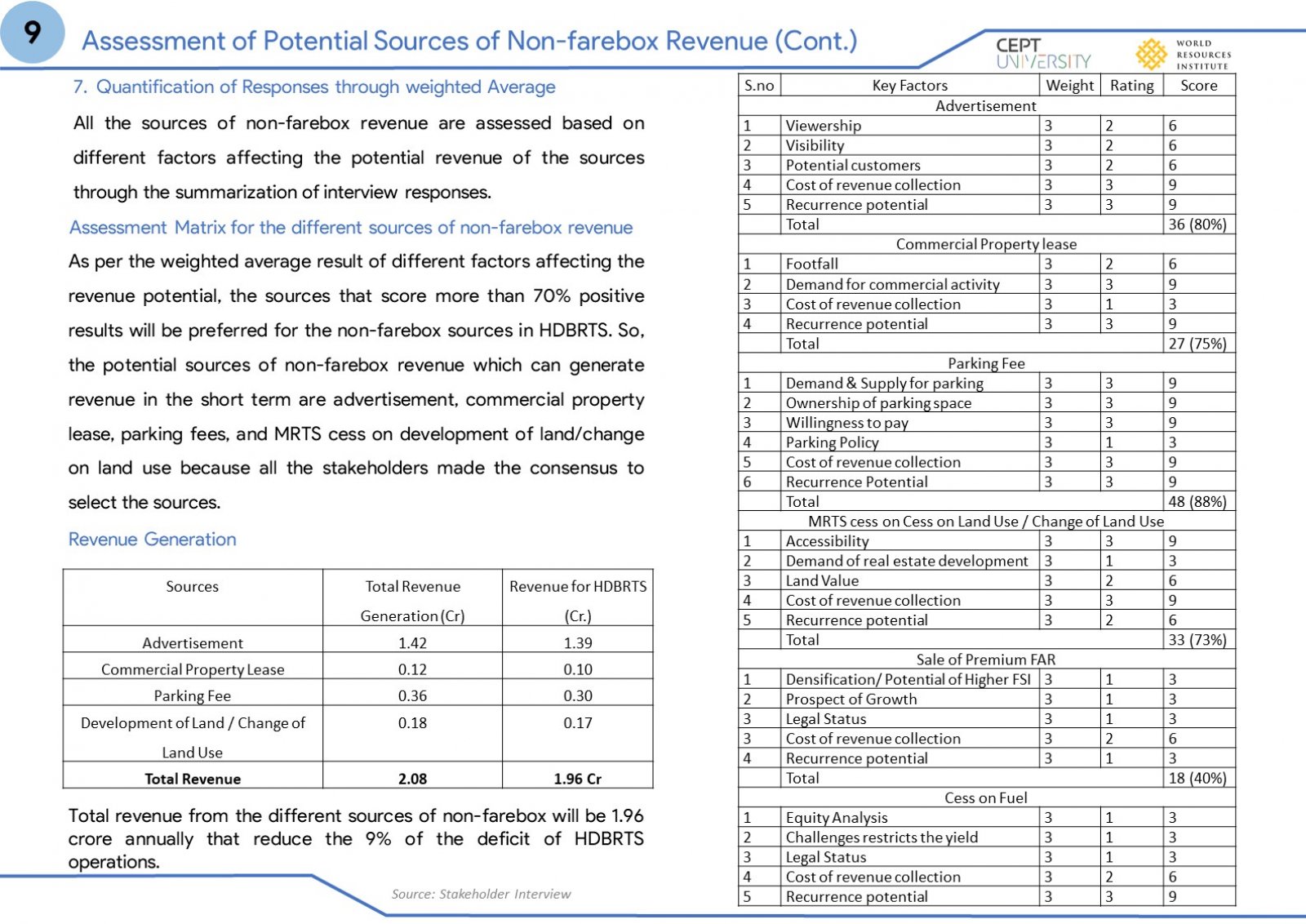

India is rapidly urbanising; cities are expected to accommodate 41% of the Indian population by 2030, up from 31% in 2011 (Census, 2011). In India, public bus transportation is the backbone of urban mobility. For operating public transport, many Indian cities concentrate on farebox sources of finance which is typically insufficient to cover both capital and operating costs. In India's several State Urban Transport Undertakings, the viability gap is approximately 50% of income (MORTH, 2017). As a result, it is necessary to develop solutions to reduce and in the long run eliminate the deficit in order to make bus operations sustainable and efficient. Through non-farebox revenue, it is possible to reduce the losses incurred in operating public transport. Non-farebox revenue can be generated by public transport company too. But they may have limited options. Transport department of state and UDD together can create more non-farebox options to fund public transport. This research aims to explore and evaluate the potential sources of non-farebox revenue to develop innovative financing mechanisms for BRTS operations in the case of Hubli-Dharwad. The objectives of the research are to identify and study the different non-farebox revenue mechanisms currently used for public transportation in Indian cities and globally for example-tax-based instruments, various user charges and land-based mechanisms, etc., to identify issues in the current financial process of BRTS operations in Hubli-Dharwad and to outline strategies for developing long-term financial resources for its efficient and effective operations. Diverse non-farebox revenue sources were examined using various Indian and global literature and case studies pertaining to bus-based public transportation systems. The existing Hubli-Dharwad BRTS finance system was then studied to investigate the last three years' annual financial status through reports and stakeholder interviews. The existing HDBRTS revenue sources were then assessed using the Delphi method, which is based on interviews with multiple numerous stakeholders with experience in public transport finances and operations. In accordance to Delphi method multiple rounds of discussion were held with stakeholders at each level of the assessment to produce fair results. Based on their responses, a weighted average was calculated, and revenue sources were divided into three categories: • Direct beneficiaries, • Polluter-pays • Indirect beneficiaries.The research findings indicate that non-farebox revenue contributes 3% of the current operation deficit in Hubli-Dharwad BRTS, however yield limits and limited authority of HDBRTS for few sources limit the opportunity to maximise it. The research further indicates that since the entire financial gap cannot be recovered with non-farebox revenue sources, HDBRTS requires additional measures to optimise its cost of operation as well as operational support from the state.